27 / 112

27 / 112

Within the beef and pork industries on the other hand, the share of

imports in domestic consumption has remained relatively constant,

whereas the share of imports in domestic lamb consumption has de-

clined. Over the course of the next decade, continuous depreciation

in the exchange rate will support the competitiveness of these net

importing industries and the share of imports in domestic consump-

tion is projected to decline for all industries except chicken (Graph 1).

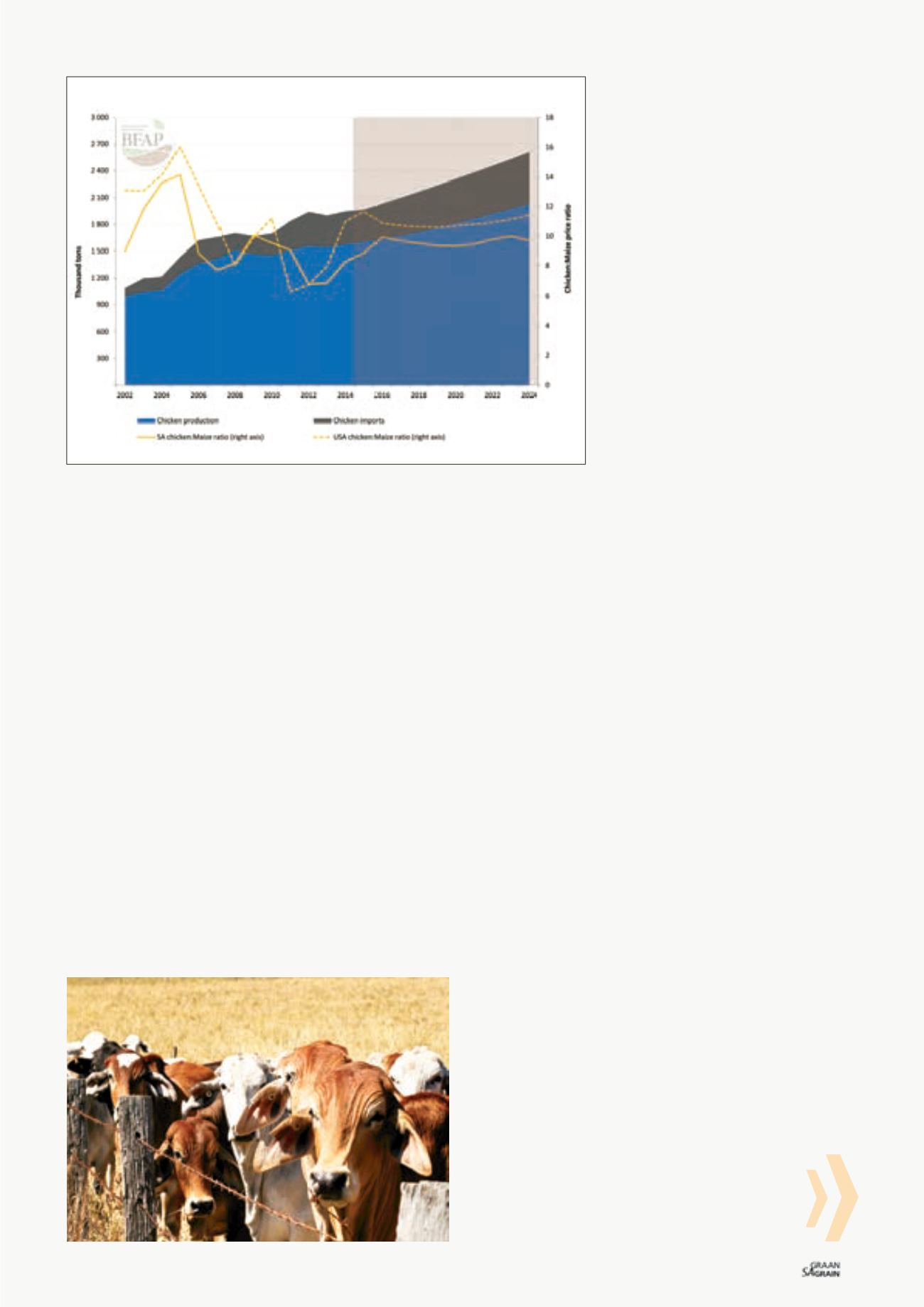

The intensive use of feed grains renders chicken production particu-

larly sensitive to high and volatile feed grain prices and hence profit-

ability has been under severe pressure over the past three years.

Maize represents the single largest ingredient in a typical feed ration

and hence the chicken to maize price ratio presented in

Graph 2

is

often used as an indicator of profitability within the industry.

The cost of soya oilcake is however also important to consider, as

it represents the main source of protein in chicken feed rations. De-

spite rapidly increasing soya oilcake production, a significant share

of the domestic soya oilcake requirement in South Africa is still be-

ing imported. Therefore the cost of feed tends to be higher than in

countries such as Brazil and the USA, which are net exporters of both

maize and soybean meal.

Nonetheless, the expansion of domestic chicken production that

accompanied favourable chicken to meat price ratios from 2002 to

2006 is clearly evident from Graph 2, whereas production has re-

mained fairly stagnant since 2011 when chicken to meat price ratios

dropped to record lows on the back of the drought induced spike in

global maize prices.

Graph 2: Outlook for the South African chicken industry.

A significant recovery in profitability has

been evident globally following the decline

in global maize prices, yet South African

producers will again face higher feed prices

than their international counterparts in 2015

due to the current drought conditions. None-

theless, persistently high international meat

prices, combined with depreciation in the

exchange rate, have supported meat prices,

and profitability ratios remain above the lev-

els observed over the past three years.

Over the course of the next decade, meat

to maize price ratios will stabilise at a

favourable level relative to the recent past

which, combined with the rapid expansion

of domestically produced soybean meal, re-

sults in a projected growth of just over 30%

in domestic chicken production. Despite this

growth, imports continue to expand, as op-

timal carcass valuation and limited demand

for bone-in portions in developed regions

such as the USA and the EU allows such

portions to be imported at very competitive

prices. Furthermore, the recent agreement

with the USA, which will allow 65 000 tons

of bone-in portions into South Africa – free

of the current anti-dumping duty of R9,40/kg – will impact on price

levels and could therefore result in a marginally slower production

growth outlook.

In contrast to chicken, beef production exhibits greater flexibility in

the feeding system, yet production remains vulnerable to changes

in weather conditions and with prices determined largely as a func-

tion of domestic supply and demand conditions, the market is often

very volatile. Drought conditions in South Africa and neighbouring

countries resulted in a sharp increase in production in 2013 and while

a return to more favourable beef to maize price ratios in 2014 point

to improved profitability, no decline was evident in slaughter

numbers, indicating that producers have yet to enter a phase of

herd rebuilding.

Supported by increasing exports of high value beef cuts following

South Africa’s recognition as free of foot and mouth disease, prices

have remained firm however, despite high slaughter volumes. None-

theless, persistent drought conditions have increased the cost of in-

tensive beef production in 2015 and while beef prices have reached

record levels, producer margins remain tight.

Graph 3

illustrates that historically, South African producers com-

pete well in the global context and under the assumption of normal

weather conditions and beef to maize price ratios are projected

to remain favourable over the coming decade. Exports more than

doubled in 2014 and while the growth is from a small base, contin-

ued depreciation of the exchange rate will likely allow South Africa

to remain competitive in these export markets, supporting domes-

tic price levels if the present foot and mouth disease free status

is maintained.

Within the context of higher prices however, the potential premi-

um that can be obtained for extensive beef production (grass fed,

hormone free) is reduced and in a cycle of lower feed grain pric-

es, the prevalence of intensive production systems (feedlots) that

convert feed to meat more efficiently is expected to increase. This

trend is already evident in a recent survey conducted by the South

African Feedlot Association, which showed an increasing number

of smaller, privately operated feedlots entering the market, a sce-

nario which will increase the demand for products consumed in the

animal feed market.

In conclusion, the 2015 edition of the BFAP Baseline presents a posi-

tive outlook for livestock production in South Africa over the next

decade, which will in turn stimulate the demand for feed products.

October 2015

25