83 / 108

83 / 108

81

August 2018

consumption as malt, sorghum meal and

sorghum rice and is successfully used as

a substitute for maize as an energy source.

Over the past three years the average an-

nual commercial consumption of sorghum

was approximately 171 500 tons, of which

155 600 tons were utilised for human con-

sumption (as malt and meal) and 8 700 tons

for animal feed. The average share of the

food market in total sorghum consumption

over the past three years is approximately

94% - 95%, of which the biggest percentage

is for meal.

Graph 1

depicts total local grain sor-

ghum consumption and production from

1997/1998 to 2018/2019, in marketing sea-

sons. The downward trend in both con-

sumption and production is very worrying

for industry role-players and the downward

trend in consumption has been identified as

one of the single most important aspects

which needs to be addressed to establish

growth in the industry. The annual com-

mercial consumption of sorghum during

the 1997/1998 marketing season was ap-

proximately 266 500 tons. This decreased

with a calculated 115 200 tons to the current

total consumption of 151 300 tons. The con-

cern is that with the present rate of decline,

sorghum may in the near future not be con-

sumed anymore.

The total sorghum production in South

Africa also decreased from 355 000 tons

during the 1997/1998 season to 83 070 tons

in the 2018/2019 production season, which

is the second smallest crop to date. The

smallest crop occurred two season ago

– when South Africa was challenged with

a terrible drought. This constitutes a de-

crease of 271 930 tons during this period.

From Graph 1 it is clear that sorghum pro-

duction in South Africa is also in a constant

downward trend.

Nutritional value

Table 1

displays the nutritional values of

sorghum compared to substitute products.

The nutritional values per 100 g of sorghum

porridge (Mabella) are compared with those

for 100 g of rice, super maize meal, bread,

millet and potatoes.

Sorghum has additional nutritional benefits

compared to the other products – it con-

tains the highest zinc and iron per serving

which proves that sorghum has numerous

health benefits and has a big role to play in

a balanced and diverse diet (BFAP, 2018).

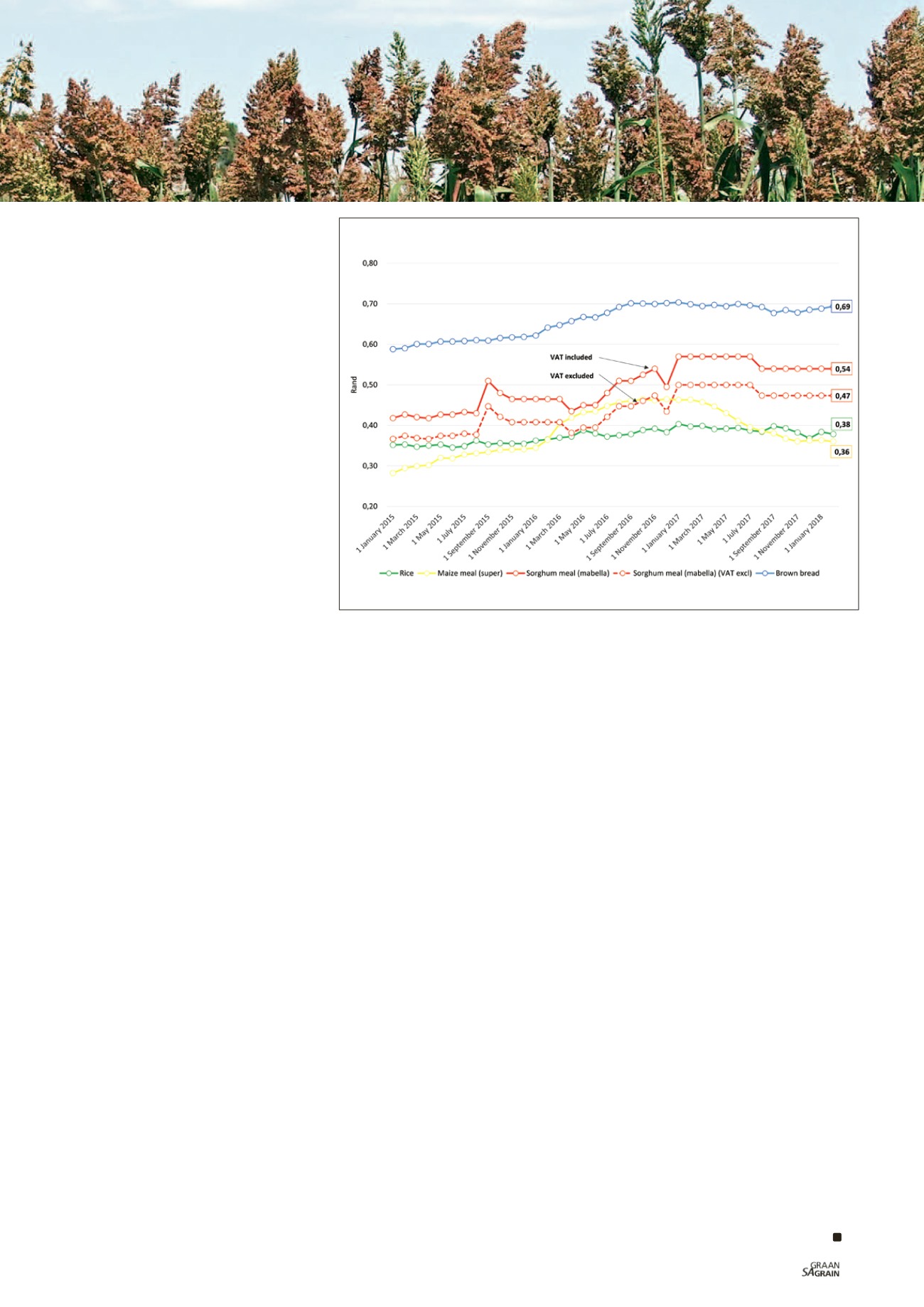

Graph 2

shows the cost (R) per 100 g

serving unit of sorghum meal compared to

super maize meal, bread and rice. It is again

clear that sorghum meal is more expensive

compared to the substitute products due

to the VAT on sorghum meal. The graph

also illustrates how the price of sorghum

meal will compare against the other pro

ducts in case the VAT on sorghum were to

be removed.

Diversify within the

same food basket

The economic climate is an important de-

terminant of consumer demand preferen

ces and consumers easily switch to

cheaper substitute products such as maize

meal and rice. It is important to broaden

the product range for consumers in lower

income groups. Sorghum is a good alterna-

tive product.

With the removal of the VAT, sorghum and

sorghum products will be able to compete

against substitute products in the zero-

rated value chain. As sorghum products

currently need to compete with substitute

products on a price basis, with the VAT re-

moval consumers will have a bigger base of

products to choose from.

It is expected that with the removal of the

VAT, sorghum’s competitiveness will im-

prove compared to that of other products

and have a positive impact on the consump-

tion of sorghum as a substitute product.

Sorghum trade

perspective

South Africa used to be a net exporter of

sorghum, but is, specifically the past few

years, becoming more dependent on im-

ports to fulfil our local demand. Every sea-

son when insufficient volumes of sorghum

is locally produced South Africa needs to

imports sorghum – currently mostly from

the USA. The ultimate aim should be to

be ‘self-sufficient’ and to have a good bal-

ance between local consumption and local

production. Hopefully, with the removal of

the VAT, this situation will change.

Conclusion and appeal

Although Grain SA hopes that sorghum

will be zero-rated, we believe that the re-

moval of the VAT would be of advantage not

only to low-income consumers, but to all

South Africans as sorghum is an indigenous

crop to Africa and is mainly used as a tradi-

tional staple food by many South Africans.

Grain SA applied for the zero-rating of sor-

ghum and sorghum meal in order to grant

the industry the opportunity to revitalise

itself and to boost the consumption of the

product. The successful turnaround of the

sorghum industry, with government sup-

port, may prevent further job losses and

economic development opportunities. The

outcome of this will be communicated.

Graph 2: Cost per single serving unit, 100 g (R).

Source: BFAP, 2018

Grain SA/Sasol photo competition