46 / 92

46 / 92

April 2015

44

ON FARM LEVEL

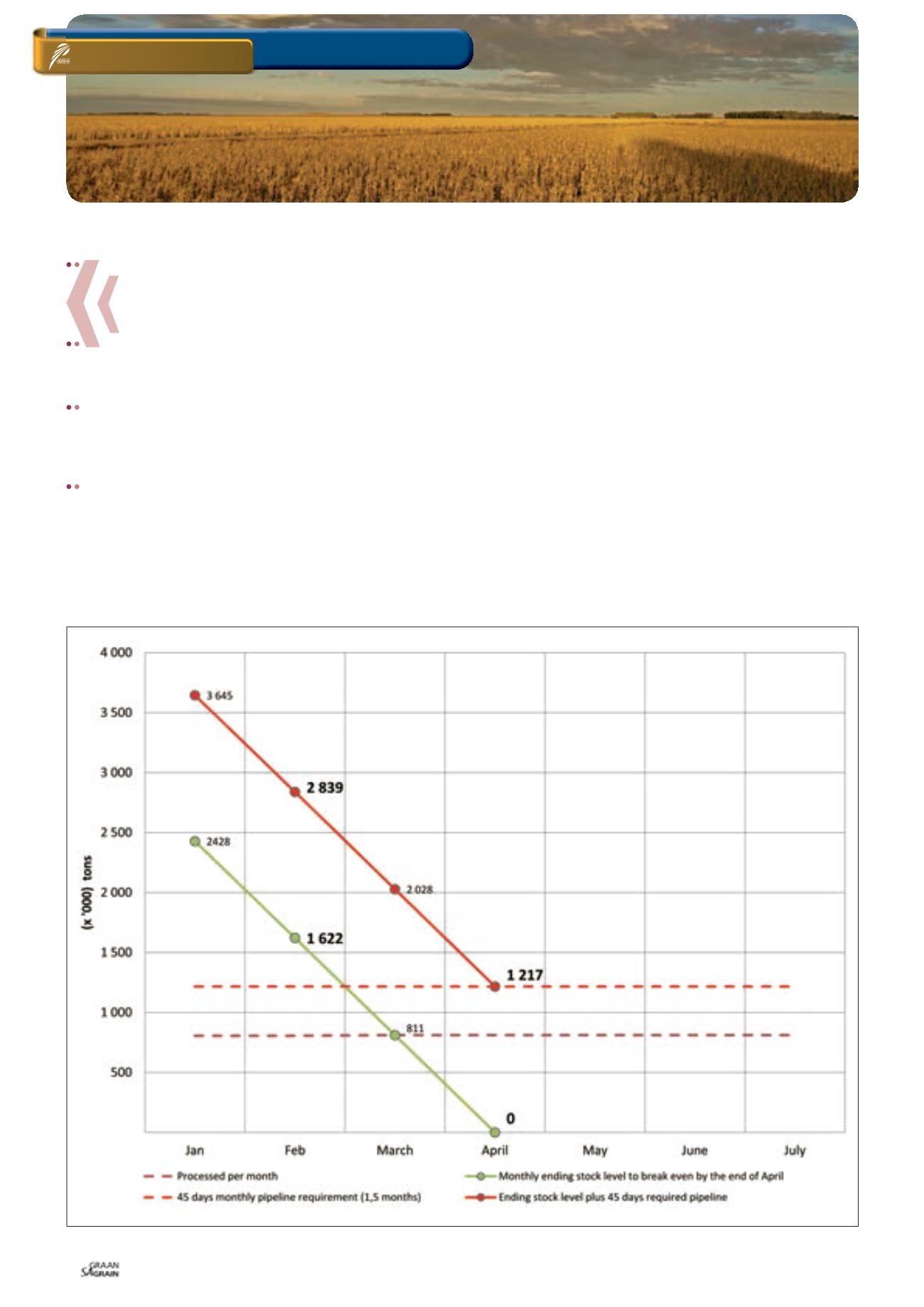

The 45 days pipeline requirement is very important in deter-

mining the import needs of the country. As soon as it seems

that the projected stock levels will be insufficient to cover the

45 days required pipeline, imports are considered by role-play-

ers and prices trend towards import parity.

Take note that stock levels were the lowest during April, but on

occasion even May. Therefore the available stocks were meas-

ured against a breakeven point above the pipeline requirement

of 45 days on 30 April of each year.

The pipeline requirement of 45 days needs to break even with

consumption on 30 April at 0. Therefore the pipeline requirement

of 45 days on the 28th of February needs to break even with

the remaining consumption for two additional months until

breaking even on 30 April.

Lastly, early deliveries during March and April decrease the pipe-

line requirement of 45 days to break even at the end of April.

It can be graphically illustrated as shown in

Graph 1

.

Population growth and maize demand

The Abstract of Agricultural Economics database indicates that

South Africa’s population growth increases by 1,3% per year. SAGIS

data indicate a growth in consumption of about 2,8% per year. See

Table 3

.

According to the NAMC, for every 1% increase in the price of maize,

the price of maize meal only increases by 0,33%. The price increase

in maize meal also took place with a lag of four months after the

price of maize starts to increase.

Prices of maize meal start to recover after about eight months

since the price of maize started to decline. Therefore it can be ex-

pected that the increase in maize prices during February will lead

to higher maize meal prices from June onwards. The limitation

on available white maize for the feed market was substituted with

possible yellow maize imports.

According to a study by the NAMC, the price of maize meal in-

creases by 0,33% for every 1% increase in the price of maize. The

average white maize price during January aimed at R2 019/ton.

The average price in February increased to R2 553/ton due to the

drought. The difference represents an increase of about R534/ton

or 26%. Based on these assumptions, the price of maize meal is

Graph 1: Ending stock levels plus pipeline requirement to break even by end of April (early producer deliveries were excluded).

GRAIN MARKET-OVERVIEW

SA Grain/

Sasol Chemicals (Fertiliser) photo competition