34 / 72

34 / 72

FOCUS

Money matters and financial services

Special

Mei 2016

32

Producers advised to view

agriculture as an investment vehicle

A

lthough agriculture has always been the backbone of most

rural economies, it can become a social and financial in-

vestment vehicle capable of driving positive change at

national and regional levels.

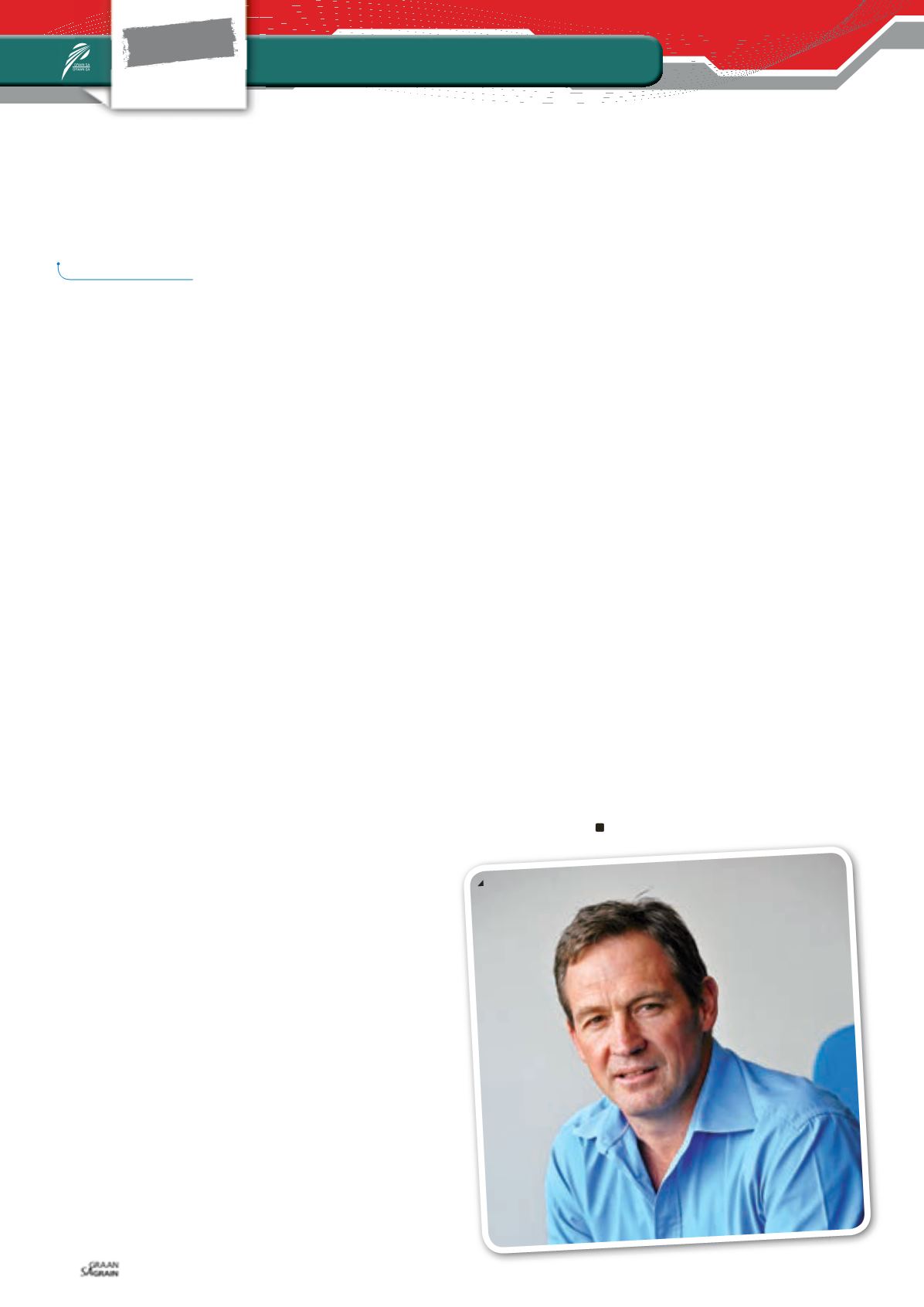

Mr Nico Groenewald (head: Agribusiness SA, Standard Bank) en-

courages primary producers to take this long-term view rather

than being caught up in the immediate crisis of the country’s worst

drought in 80 years.

‘All of us in agriculture know that it is a cyclical sector and that weath-

er is a fundamental, but unpredictable factor, for which we must con-

tinuously evolve better strategies.

‘It is also the one sector that is critical to human survival. People

must eat. However, partly because of the weather and often in spite

of it, the ways of ensuring that people get good quality, nourishing

food are evolving. So, if you’re in agriculture, you’re going to be a

contributor to one of the most profound evolutions ever to influence

humanity’s future. Choosing the way you do that calls for wisdom

and vision.

‘This is not just a financial consideration; it also has immense so-

cial implications. It will shift agriculture into the domain of social in-

vestment, whereby people invest not only for a financial return, but

also to ensure that society functions more equitably as a result of

their input.

‘For all sorts of reasons, therefore, it’s time for producers to look at

the work they do as a type of investment vehicle.

‘That sounds theoretical. In fact, it’s extremely practical. New

agricultural strategies are giving rise to new up- and downstream

business opportunities in which conventional investors can be per-

suaded to take a stake. Producers can either create the investment

opportunities or participate in them. Either way, they gain a share

of the value chain upside that they don’t currently have. It also ena-

bles them to influence the direction in which agriculture evolves and,

thereby, how effectively it serves both producers and humanity.

‘For most producers, however, with or without drought conditions,

funding remains a challenge. Again, the solution lies in looking at

agriculture as an investment vehicle rather than purely as a tacti-

cal, operational exercise undertaken season by season,’ Groenewald

mentioned.

‘In an investment scenario, banks and their relationship managers

and agricultural economists can be a significant ally. In recent years,

and particularly since the economic crisis of 2008 that was triggered

by the bad behaviour of some banks, there has been a tendency to

view banks with suspicion.

‘However, tighter regulatory environments are keeping bankers with

an urge for experimentation, under strict control. Experience proves

that smaller banks are no less subject to flaws than the big ones and

that, actually, the big ones can bring more effective and longer-term

funding resources to bear as agriculture becomes more globalised.

‘In fact, agriculture has owed most of its operations to the loans

made available by large banks from the time of the establishment of

the world’s oldest bank in Italy, on the basis of a statute regulating

agricultural and pastoral activities in the region.

‘That said, modern funding trends driven largely by technology and

new phenomena such as crowd sourcing and crowd funding are

making other financing options available to players in the agricul-

tural value chain.

‘Producers wanting to take an investment approach should stick to

the basics of financing, as proven by banks,’ he said.

He cited by means of an example the potential of positive financial

leverage, in which assets acquired with funds provided by share-

holders or via a bank loan generate a rate of return higher than the

rate of interest or the dividend payable to the providers of funds.

The linkages between the use of debt as leverage, its impact on fi-

nancial risk, and the understanding of cash cycles and free cash are

some of the aspects which banks analyse in their risk assessments

and thus can provide valuable input to farming businesses with po-

tential expansion, capital replacement, and new venture decisions.

In addition to actual funding, banks with agricultural business units

provide ancillary services that can help producers achieve a com-

petitive advantage and mitigate their risks. These include access

to specialists focusing on financial viability, repayment ability and

appropriate debt restructuring, agricultural market trend and infor-

mation services, agricultural publications, value chain funding solu-

tions, and tangible support of organised agriculture.

‘Banks are in the business of creating wealth,’ Groenewald conclud-

ed. ‘But they can do that only through entrepreneurs who invest in

themselves and the future. We believe it’s time for producers to be

such entrepreneurs.’

Product information

STANDARD BANK

Nico Groenewald