- Follow us:

- Our Commodities:

-

December 2015

|

1. Accounting policy and presentation The annual consolidated financial statements have been prepared in accordance with the International Financial Reporting Standard for Small and Mediumsized Entities. The consolidated financial statements are prepared on the historical cost basis. They are presented in South African rands. The accounting policy is consistent with the prior period. 1.1 Significant judgements and sources of estimation uncertainty In preparing the annual consolidated financial statements, management is required to make estimations and assumptions that affect the amounts represented in the annual consolidated financial statements and related disclosures. Use of available information and the application of judgement is inherent in the formation of estimates. Actual results in the future could differ from these estimates which may be material to the annual consolidated financial statements. Significant judgements include: Loans and receivables The impairment for loans and receivables are calculated on a portfolio basis, based on historical loss ratios, adjusted for national and industry specific economic conditions and other indicators present at the reporting date that correlate with defaults on the portfolio. These annual loss ratios are applied to loan balances in the portfolio and scaled to the estimated loss emergence period. Fair value estimate The fair value of financial instruments that are not in an active market (for example, counter derivatives) is determined by using valuation techniques. The entity uses a variety of methods and assumptions that are based on market conditions existing at each reporting date. Quoted market prices or dealer quotes for similar instruments are used for long-term debt. Other techniques, such as estimated discounted cashflows, are used to calculate the fair value for the remaining financial instruments. The fair value of forward exchange contracts is calculated using the quoted exchange rate on reporting date. It is considered that the carrying value less impairment of trade receivables and trade payables equal their fair value. The fair value of financial liabilities for disclosure purposes is estimated by discounting the future contractual cashflows at the current market interest rate that is available to the entity for similar financial instruments. 1.2 Provisions Provisions are made by management on the basis of available information. 1.3 Property, plant and equipment The cost of an item of property, plant and equipment is recognised as an asset when:

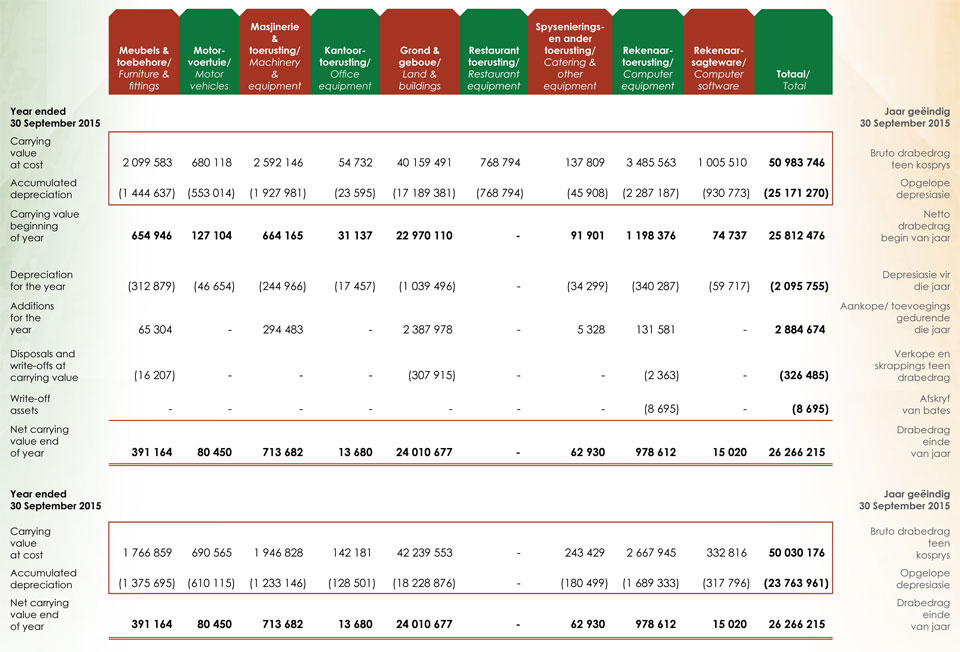

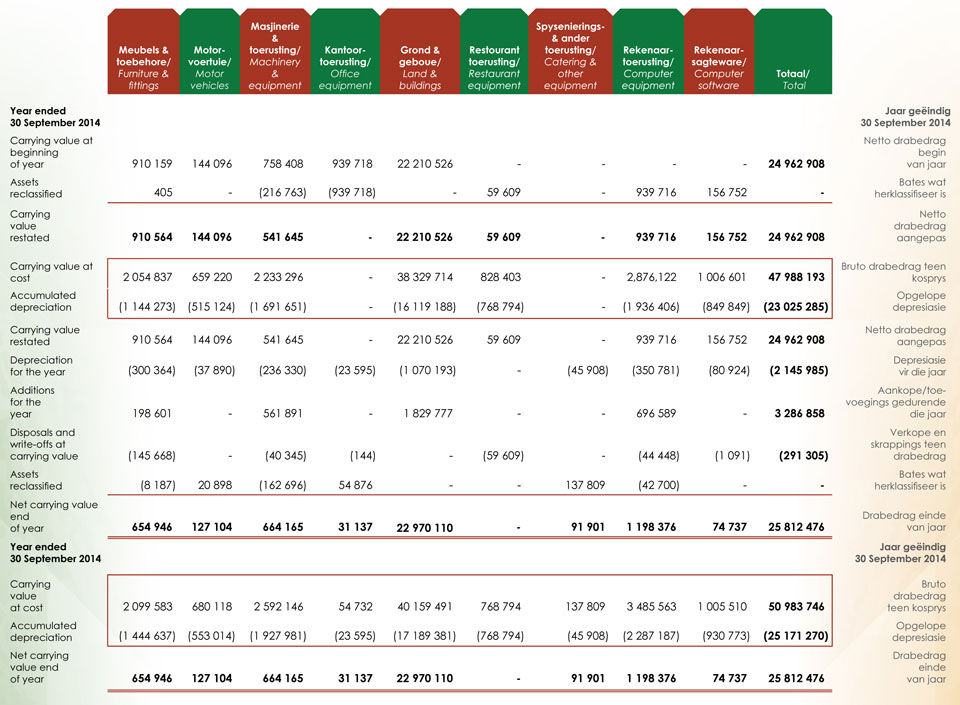

Property, plant and equipment is initially measured at cost. Costs include costs incurred initially to acquire or construct an item of property, plant and equipment and costs incurred subsequently to add to, replace part of, or service it. If a replacement cost is recognised in the carrying amount of an item of property, plant and equipment, the carrying amount of the replaced part is derecognised. All other repairs and maintenance are charged to the statement of comprehensive income during the financial period in which they are incurred. The initial estimate of the costs of dismantling and removing the item and restoring the site on which it is located is also included in the cost of property, plant and equipment. Property, plant and equipment is carried at cost less accumulated depreciation and any impairment losses. The depreciation rate of items of property, plant and equipment have been assessed as follows:

The residual value, useful life and depreciation method of each asset is reviewed, and adjusted if appropriate, at the end of each reporting period. If the expectations differ from previous estimates, the change is accounted for as a change in accounting estimate. Each part of an item of property, plant and equipment with a cost that is significant in relation to the total cost of the item is depreciated separately. The depreciation charge for each period is recognised in profit or loss unless it is included in the carrying amount of another asset. The gain or loss arising from derecognition of an item of property, plant and equipment is included in profit or loss when the item is derecognised. The gain or loss arising from derecognition of an item of property, plant and equipment is determined as the difference between the net disposal proceeds, if any, and the carrying amount of the item. An asset's carrying amount is written down immediately to its recoverable amount if the asset's carrying amount is greater than its estimated recoverable amount. 1.4 Investments in subsidiaries In the entity's separate financial statements, investments in subsidiaries are carried at fair value, with changes in fair value recognised in profit and loss. 1.5 Financial instruments Trade receivables The carrying amount of the asset is reduced through the use of an allowance account, and the amount of the loss is recognised in profit or loss within operating expenses. When a trade receivable is uncollectable, it is written off against the allowance account for trade receivables. Subsequent recoveries of amounts previously written off are recognised in other income. Trade receivables are classified as financial assets that are debt instruments measured at amortised cost. Trade payables Trade payables are classified as financial liabilities measured at amortised cost Cash and cash equivalents Cash and cash equivalents are classified as financial assets that are debt instruments measured at amortised cost. 1.6 Leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease if it does not transfer substantially all the risks and rewards incidental to ownership. Operating leases – lessee Any contingent rent is expensed in the period they are incurred. 1.7 Inventory Inventories are measured at the lower of cost and net realisable value. Net realisable value is the estimated selling price in the ordinary course of business, less the estimated costs of completion and the estimated costs necessary to make the sale. The cost of inventories comprises of all costs of pur-chase, costs of conversion and other costs incurred in bringing the inventories to their present location and condition. The cost of inventories is assigned using the weighted average cost formula. The same cost formula is used When inventories are sold, the carrying amounts of those inventories are recognised as an expense in the period in which the related revenue is recognised. The amount of any write-down of inventories to net realisable value and all losses of inventories are recognised as an expense in the period the write-down or loss occurs. The amount of any reversal of any write-down of inventories, arising from an increase in net realisable value, are recognised as a reduction in the amount of inventories recognised as an expense in the period in which the reversal occurs. 1.8 Trust funds Congress decides for which expenses the levy fund and relief fund may be used, as well as the transfers to and from the levy fund and relief fund. 1.9 Employee benefits Short-term employee benefits The expected cost of compensated absences is recognised as an expense as the employees render services that increase their entitlement or, in the case of non-accumulating absences, when the absence occurs. The expected cost of profit sharing and bonus payments is recognised as an expense when there is a legal or constructive obligation to make such payments as a result of past performance. 1.10 Provisions and contingencies Provisions are recognised when:

The amount of a provision is the present value of the expenditure expected to be required to settle the obligation. Where some or all of the expenditure required to settle a provision is expected to be reimbursed by another party, the reimbursement shall be recognised when, and only when, it is virtually certain that reimbursement will be received if the entity settles the obligation. The reimbursement shall be treated as a separate asset. The amount recognised for the reimbursement shall not exceed the amount of the provision. Provisions are not recognised for future operating losses. If an entity has a contract that is onerous, the present obligation under the contract shall be recognised and measured as a provision. 1.11 Revenue Revenue is defined as external trusts or government institution allocation, advertising and printing costs received, subscription fee, membership fees received, commodity levies received, management fees received, farm income, harvest day receipts, sponsorships, rental income, as well as other sundry operating income. When the outcome of a transaction involving the rendering of services can be estimated reliably, revenue associated with the transaction is recognised by reference to the stage of completion of the transaction at the balance sheet date. The outcome of a transaction can be estimated reliably when all the following conditions are satisfied:

When the outcome of the transaction involving delivery can not be reliably calculated, the revenue is recognised only in respect of the expenses recognised that are recoverable. Revenue is measured at the fair value of the consideration received or receivable and represents the receivables for goods and services in the ordinary course of business provided, net of trade discounts and quantity discounts and value added tax. Interest is recognised in profit or loss using the effective interest rate method. Dividends are recognised in profit or loss when the entity's right to receive payment is established. Voluntary contributions, such as charges, members' fees, donations and grants for specific projects are recognised when received. Rental income received is recognised in the statement of comprehensive income on a straight-line basis over the lease term. 1.12 Borrowing costs Borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying asset are capitalised as part of the cost of that asset until such time as the asset is ready for its intended use. The amount of borrowing costs eligible for capitalisation is determined as follows:

The capitalisation of borrowing costs commences when:

Capitalisation is suspended during extended periods in which active development is interrupted. Capitalisation ceases when substantially all the activities necessary to prepare the qualifying asset for its intended use or sale are complete. All other borrowing costs are recognised as an expense in the period in which they are incurred. 1.13 Income tax The income tax status of the Grain SA Group entities is as follows: In terms of the Income Tax Act, Grain SA is exempt NAMPO Geboue (Pty) Ltd is a taxpayer entity. Current tax assets and liabilities Deferred tax assets and liabilities A deferred tax asset is recognised for all deductible temporary differences and for the carry forward of unused tax losses and unused tax credits. Deferred tax assets and liabilities are measured at the tax rates that are expected to apply to the period when the asset is realised or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted by the reporting date. Tax expenses 1.14 Consolidation policy The consolidated annual financial statements include the assets and liabilities of all entities and their results for the period. The abovementioned are entities where Grain SA has the power to govern or control the entity's financial and operating policies so as to obtain benefits from its activities, and include:

Consolidation comprises the following:

|

1. Aanbieding van finansiële jaarstate Die gekonsolideerde finansiële jaarstate is ooreenkomstig die Internasionale Finansiële Rapporteringstandaarde vir Klein en Mediumgrootte Ondernemings opgestel. Die gekonsolideerde finansiële jaarstate is op die historiesekoste-grondslag opgestel. Dit word in Suid-Afrikaanse rand aangebied. Die rekeningkundige beleid stem ooreen met die vorige tydperk. 1.1 Beduidende ramings en bronne van skattingsonsekerheid Met die opstel van die gekonsolideerde finansiële jaarstate moet die bestuur sekere ramings en veronderstellings maak wat die bedrae kan beïnvloed wat in die gekonsolideerde finansiële jaarstate weerspieël word, sowel as verwante openbaarmakings. Die gebruik van beskikbare inligting en die toepassing van oordeel is eie aan ramings. Die werklike toekomstige resultate kan van dié ramings verskil, wat van wesenlike belang vir die gekonsolideerde finansiële jaarstate kan wees. Belangrike ramings sluit in: Lenings en debiteure Die waardedaling vir lenings en debiteure word op 'n portefeulegrondslag bereken, gegrond op historiese verliesverhoudings wat aangepas is vir nasionale en bedryfspesifieke ekonomiese toestande en ander aanduiders op die verslagdoeningsdatum wat met gebreke in die portefeulje verband hou. Dié jaarlikse verliesverhoudings word toegepas op leningsaldo's in die portefeulje en volgens skaal by die beraamde verliesvoorkomstydperk aangepas. Billikewaarde-raming Die billike waarde van finansiële instrumente wat nie Gekwoteerde markpryse of handelaarkwotasies vir soortgelyke instrumente word vir langtermynskuld gebruik. Ander tegnieke, soos beraamde verdis-konteerde kontantvloei, word gebruik om billilke waarde vir die oorblywende finansiële instrumente te bereken. Die billike waarde van vooruitvalutakontrakte word bereken deur gekwoteerde vooruitwisselkoerse op die verslagdoeningsdatum te gebruik. Daar word geag dat die drawaarde minus waardedalingsvoorsiening van debiteure en handels krediteure bykans hul billike waarde is. Die billike waarde van finansiële aanspreeklikhede vir openbaarma-kingdoeleindes word beraam deur die toekomstige kontraktuele kontantvloei te verdiskonteer teen die huidige markrentekoers wat vir soortgelyke finansiële instrumente aan die entiteit beskikbaar is. 1.2 Voorsienings Voorsienings is gemaak en die bestuur het op grond van die beskikbare inligting 'n raming gedoen. 1.3 Eiendom, aanleg en toerusting Die koste van eiendom, aanleg en toerusting word as 'n bate erken wanneer:

Eiendom, aanleg en toerusting word aanvanklik teen kosprys erken. Koste sluit in koste wat aanvanklik aangegaan is om 'n item van eiendom, aanleg en toerusting te verkry of op te rig en koste wat daarna aangegaan is om aan te bou, 'n deel daarvan te vervang of dit te diens. Indien 'n vervangingskoste in die drabedrag van 'n item eiendom, aanleg en toerusting erken word, word die drabedrag van die vervangingskoste omgeswaai. Alle ander herstel- en instandhoudingskostes word in die staat van omvattende inkomste erken gedurende die finansiële periode waarin die uitgawe aangegaan is. Die aanvanklike raming van die koste om die items af te breek en te verwyder en die perseel waarop dit geleë is te herstel, word ook by die koste van masjinerie en toerusting ingesluit. Eiendom, aanleg en toerusting word teen kosprys Die depresiasiekoers van eiendom, aanleg en toerusting is soos volg:

Die reswaarde, nutsduur en depresiasiemetode van elke bate word aan die einde van elke verslagdoeningstydperk nagesien. Indien die verwagting van vorige ramings verskil, word die verandering as 'n verandering in rekeningkundige raming in berekening gebring. Elke deel van 'n item van eiendom, aanleg met 'n koste wat in verhouding tot die totale koste van die item beduidend is, word afsonderlik gedepresieer. Die depresiasiekoste vir elke tydperk word in wins of verlies erken tensy dit by die drabedrag van 'n ander bate ingesluit is. Die wins of verlies voortspruitend uit die verkoop van 'n item van eiendom, aanleg en toerusting word by wins of verlies ingesluit wanneer die item verkoop word. Die wins of verlies voortspruitend uit die verkoop van 'n item van eiendom, aanleg en toerusting word bereken as die verskil tussen die netto opbrengs ontvang, indien enige, en die drabedrag van die item. 'n Bate se drabedrag word dadelik afgeskryf tot en met sy verhaalbare bedrag wanneer die bate se drabedrag groter is as die beraamde verhaalbare bedrag. 1.4 Beleggings in filiale In die entiteit se afsonderlike finansiële jaarstate word beleggings in filiale gedra teen billike waarde, en veranderings in billike waarde word in wins en verlies erken. 1.5 FinansiËle instrumente Handelsdebiteure Die drabedrag van die bate word verminder deur die gebruik van 'n voorsieningsrekening en die bedrag van die verlies word in die wins of verlies in bedryfskoste erken. Wanneer 'n handelsdebiteur oninvorderbaar is, word dit afgeskryf teen die voorsieningsrekening vir handelsdebiteure. Bedrae wat voorheen afgeskryf is en daarna ingevorder word, word in ander inkomste erken. Handelsdebiteure word as finansiële bates wat 'n skuldinstrument is, geklassifiseer en gemeet teen geamortiseerde koste. Handelskrediteure Handelskrediteure word as finansiële laste geklassifiseer en gemeet teen geamortiseerde koste. Kontant en kontantekwivalente Kontant en kontantekwivalente word as 'n finansiële bate wat 'n skuld instrument is gemeet teen geamortiseerde koste. 1.6 Hure 'n Huur word as 'n bruikhuur geklassifiseer indien dit in wese al die risiko's en voordele verbonde aan eienaarskap oordra. 'n Huur word as 'n bedryfshuur geklassifiseer indien dit nie in wese al die risiko's en voordele verbonde aan eienaarskap oordra nie. Bedryfshure – huurder Enige voorwaardelike huur word erken in die tydperk waarin dit aangegaan word. 1.7 Voorraad Voorraad word teen kosprys of die netto realiseerbare waarde, welke een ook al die laagste is, gemeet. Die netto realiseerbare waarde is die beraamde verkoopsprys in die gewone gang van die besigheid minus die beraamde koste van afhandeling en die beraamde koste wat nodig is om die verkoop te doen. Die koste van voorraad bestaan uit alle verkrygingskoste, omskeppingskoste en enige ander koste wat aangegaan word om die voorraad te bring tot waar dit is en in die toestand waarin dit is. Die voorraadkoste word toegeken deur die geweegde gemiddelde kosteformule te gebruik. Dieselfde koste- Wanneer voorraad verkoop word, word die drabedrag van die voorraad as 'n uitgawe erken in die tydperk waarin die verwante inkomste erken word. Die bedrag van enige afwaartse waardasie van voorraad tot netto realiseerbare waarde en alle verliese van voorraad word as 'n uitgawe erken in die tydperk waarin die afwaartse waardasie of verlies plaasvind. Die bedrag van enige omswaai van enige afwaartse waardasie van voorraad voortspruitend uit 'n toename in netto realiseerbare waarde, word in die tydperk waarin dit omgeswaai word erken as 'n daling in die hoeveelheid voorraad wat as 'n uitgawe erken word. 1.8 Trustfondse Die Kongres besluit oor uitgawes waarvoor die heffingsfonds en regshulpfonds aangewend mag word, asook oor oorplasings na en vanaf die heffingsfonds en regshulpfonds. 1.9 Werknemervoordele Korttermynwerknemervoordele Die verwagte koste van betaalde afwesigheid word as 'n uitgawe erken na gelang die werknemer diens lewer wat sy/haar geregtigheid daarop verhoog, of in die geval van afwesigheid wat nie ophoop nie, wanneer die afwesigheid plaasvind. Die verwagte koste van winsdeling en bonusbetalings word as 'n uitgawe erken wanneer daar 'n wettige of afgeleide verpligting is om sodanige betaling as gevolg van vorige prestasie te doen. 1.10 Voorsienings en gebeurlikhede Voorsienings word erken wanneer:

Die bedrag van 'n voorsiening is die huidige waarde van die besteding wat na verwagting nodig sal wees om die verpligting na te kom. Indien 'n ander party na verwagting 'n gedeelte van of die totale besteding sal terugbetaal wat nodig sal wees om 'n voorsiening te vereffen, sal die vergoeding erken word wanneer en slegs wanneer dit bykans seker is dat vergoeding ontvang sal word indien die entiteit die verpligting nakom. Die vergoeding sal as 'n afsonderlike bate hanteer word. Die bedrag wat vir die vergoeding erken sal word, sal nie meer wees as die bedrag van die voorsiening nie. Voorsiening sal nie vir toekomstige verlies erken word nie. Indien 'n entiteit 'n kontrak het wat beswarend is, sal die huidige verpligting ingevolge die kontrak erken word en as 'n voorsiening bereken word. 1.11 Inkomste Inkomstes word gedefinieer as eksterne trusts of staatsinstansiebefondsing, advertensie en drukkostes gevorder, intekengelde, ledegelde ontvang, bedryfsheffings ontvang, bestuursfooie ontvang asook oesdagontvangstes, borgskappe, huurinkomste en ander diverse bedryfsontvangstes. Wanneer die uitslag van 'n transaksie wat dienslewering behels, betroubaar bereken kan word, word inkomste ten opsigte van die transaksie erken met verwysing na die afhandelingstadium van die transaksie op die balansstaatdatum. Die uitslag van die transaksie kan betroubaar bereken word wanneer al die volgende voorwaardes nagekom word:

Wanneer die uitslag van die transaksie wat dienslewering behels, nie betroubaar bereken kan word nie, word inkomste slegs erken ten opsigte van die erkende uitgawes wat verhaalbaar is. Inkomste word bereken teen die billike waarde van die teenprestasie wat ontvang is of ontvangbaar is en verteenwoordig die ontvangbare bedrae vir goedere en dienste wat in die normale gang van sake verskaf word, na aftrekking van handelskortings en hoeveelheidskorting en belasting op toegevoegde waarde. Rente word in wins of verlies erken deur die effektiewe rentekoersmetode te gebruik. Dividende word in wins en verlies erken wanneer die entiteit se reg om die betaling te ontvang, gevestig is. Vrywillige bydraes, byvoorbeeld heffings, ledegeld, donasies en toekennings vir spesifieke projekte word verantwoord wanneer dit ontvang word. Huurinkomste verdien word erken in die staat van omvattende inkomste op 'n reguitlyngrondslag oor die termyn van die huurkontrak. 1.12 Leenkoste Leenkoste wat regstreeks toeskryfbaar is aan die

Die kapitalisering van leenkoste neem 'n aanvang wanneer:

Kapitalisering word opgeskort vir lang tydperke waartydens aktiewe ontwikkeling onderbreek is. Kapitalisering eindig wanneer al die aktiwiteite wat nodig is om die kwalifiserende bate vir die voorgenome gebruik of verkoop daarvan, in wese afgehandel is. Alle ander leenkoste word as 'n uitgawe erken in die tydperk waarin dit aangegaan word. 1.13 Inkomstebelasting Graan SA Groep entiteite se belastingstatus is soos volg: Graan SA is ingevolge die Inkomstebelastingwet vrygestel van inkomstebelasting op ontvangstes, toevallings en skenkings. NAMPO Geboue (Edms) Bpk is 'n belastingplig- Lopendebelastingbates en -laste Uitgestelde belastingbates en -laste 'n Uitgestelde belastingbate word vir alle aftrekbare tydelike verskille erken. Uitgestelde belastingbates en -laste word bereken teen die verwagte heersende belastingkoers wanneer die bate gerealiseer word of die aanspreeklikheid vereffen word, gegrond op belastingkoerse (en belastingwette) wat teen die verslagdoeningsdatum uitgevaardig is of in wese uitgevaardig is. Belastinguitgawes 1.14 Konsolidasiebeleid Die gekonsolideerde finansiële jaarstate sluit die bates en laste van al die entiteite en hul resultate vir die periode in. Die bogenoemde is entiteite waaroor beheer deur Graan SA oor die entiteite se bedryfs- en finansiële beleid uitgeoefen kan word ten einde voordeel uit sy aktiwiteite te trek, en sluit in:

Konsolidasie behels die volgende:

|

|||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||

Publication: December 2015

Section: Financial statements